Bangladesh needs roughly 6 million additional housing units today, a figure projected to exceed 10.5 million by 2030. Nearly three-quarters of that demand sits in the affordable segment, where families build their own homes incrementally as savings allow. Buildings already account for close to 40 percent of national energy consumption, and every unit built with conventional methods locks in decades of heat stress, high operating costs, and emissions in one of the world's most climate-vulnerable countries.

The conventional view holds that green construction in Bangladesh is a premium product: relevant to boutique developers, out of reach for the self-built majority, and dependent on subsidy. New evidence from the Affordable Green Housing Market Assessment, conducted by Innovision Consulting for IFC, points to a different conclusion. Demand for green housing among ordinary households is broad, price-rational, and already ahead of the market's ability to serve it. What is missing is not willingness to build green. It is a financing product designed for how these households actually build and earn.

The assessment surveyed self-built households across Dhaka, Khulna, and Rangpur, three cities selected to represent Bangladesh's distinct climate exposures: urban heat, coastal salinity, and grid instability. The household survey was complemented by interviews with developers, contractors, masons, and building-material suppliers, and by a comparative cost analysis of conventional and green materials. Respondents were concentrated in the BDT 51,000 to 150,000 monthly income band, which represents 78 percent of the sample and the core addressable market for green housing finance. The findings on adoption and willingness to pay are stated preferences; the recommendations below are designed to convert stated demand into realized lending, not to assume the conversion.

Among surveyed households, 82.9 percent reject the proposition that green housing is a luxury, and 93.4 percent associate green homes directly with improved family health through better ventilation, cooler interiors, and cleaner indoor air. Expectations of financial value are equally consistent: nearly all respondents anticipate that green homes will command higher resale and rental values.

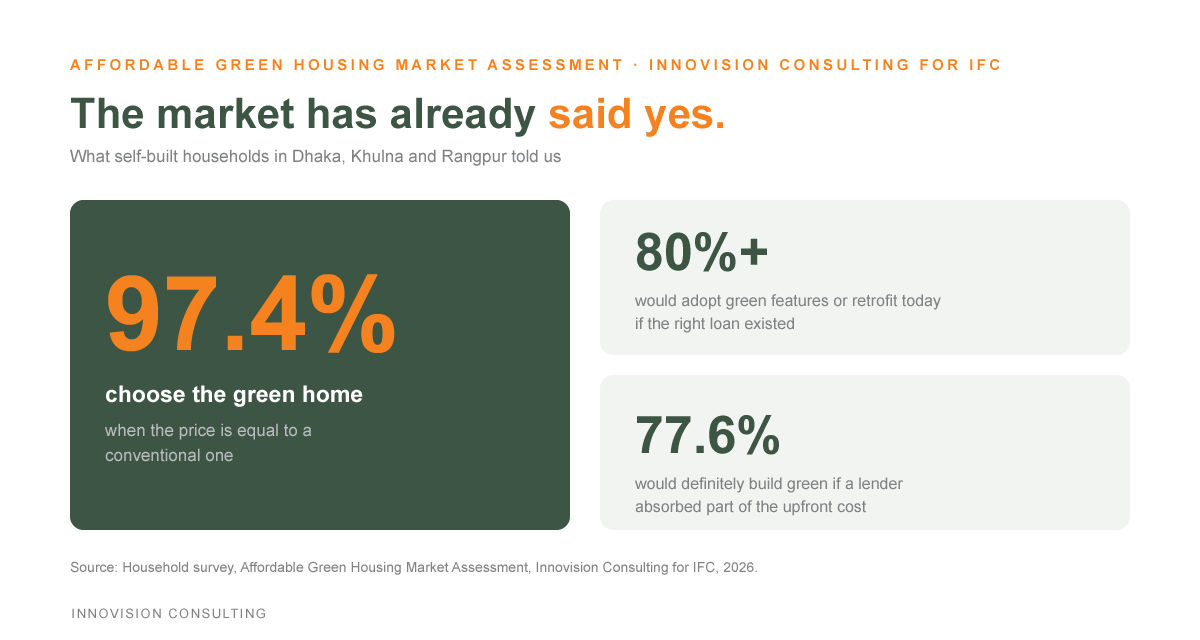

Stated adoption intent follows the same pattern. More than 80 percent of households would adopt green features or retrofit their existing home if an appropriate loan existed, 77.6 percent would definitely build green if a lender absorbed part of the upfront cost, and 97.4 percent choose the green option when prices are equal. Households are also willing to share the cost: 51.3 percent would accept a green premium of 3 to 6 percent, and a similar share could absorb an additional BDT 1,000 to 3,000 in monthly installments.

These figures sit at or above the willingness-to-pay benchmarks observed in emerging markets where green affordable housing finance has subsequently scaled. They indicate a demand base large enough to support a commercial product rather than a pilot.

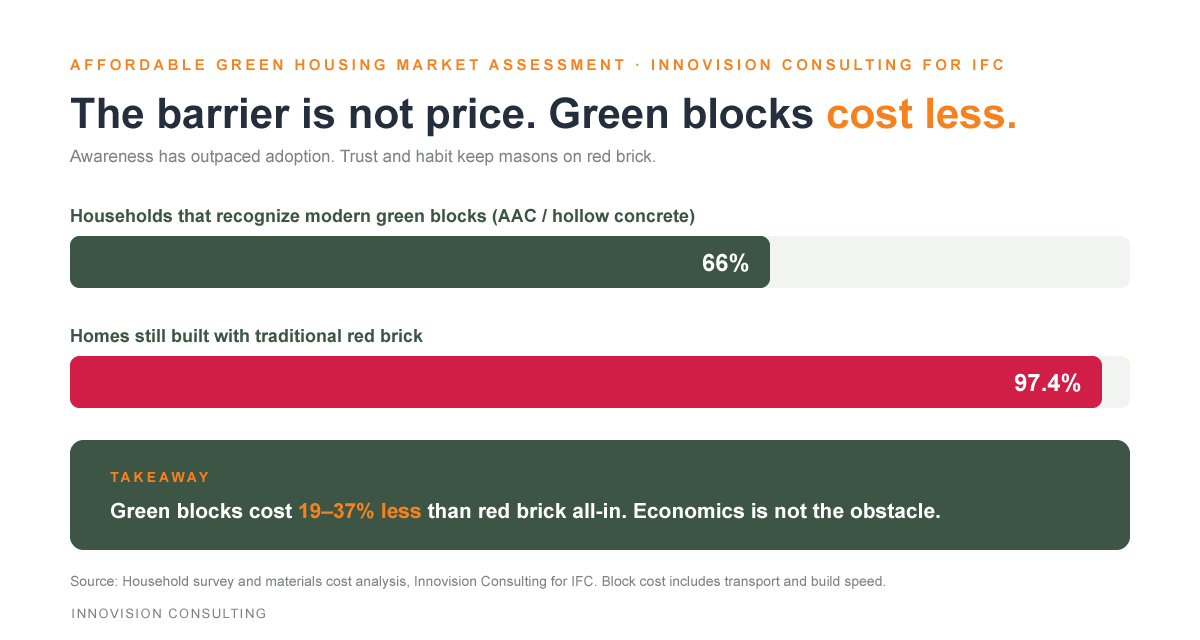

The study's most consequential finding concerns why adoption lags demand. Two-thirds of households already recognize AAC and hollow concrete blocks, yet 97.4 percent of homes continue to be built with traditional red brick, despite a cost analysis showing that green blocks are 19 to 37 percent cheaper than brick once transport and construction speed are included.

The gap is explained by the delivery system rather than the demand side. Masons and contractors default to familiar materials; certified products and skilled installers are unevenly available outside Dhaka; and households lack a trusted mechanism to verify quality. The genuine upfront-cost barrier is concentrated in systems rather than structure: rooftop solar, insulation, and efficient appliances require capital outlays before savings accrue, and many components are imported, which raises both purchase prices and required loan sizes. This import dependence is itself a market signal, pointing to an adjacent opportunity in local manufacturing of green building materials and components.

The design implication is precise. Households are not asking for cheaper credit alone: 81.6 percent want financing bundled with certified contractors, verified materials, and quality assurance, and 99 percent expect green loans to be priced below conventional mortgages. The product that unlocks this market is a loan attached to a guarantee of competent delivery.

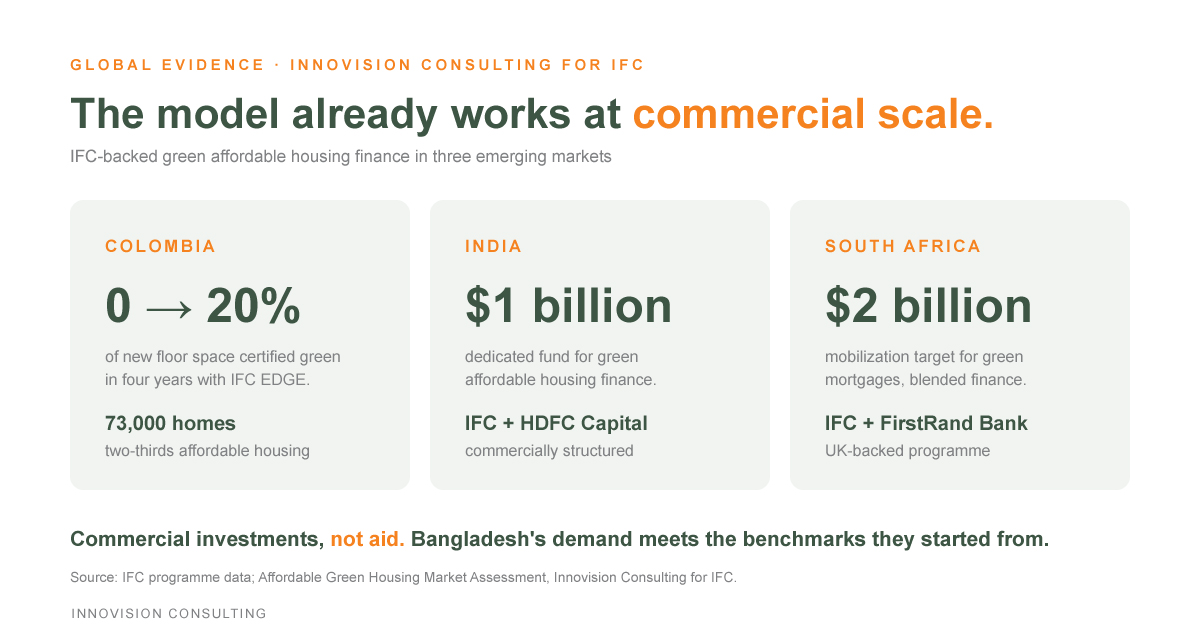

Bangladesh would be a fast follower rather than a pioneer. In Colombia, IFC's EDGE certification supported growth in the green residential market from zero to 20 percent of new floor space within four years, certifying more than 73,000 homes, two-thirds of them affordable. In India, IFC and HDFC Capital operate a $1 billion fund dedicated to green affordable housing finance. In South Africa, IFC's blended-finance partnership with FirstRand Bank targets $2 billion in mobilization for green mortgages. Each is structured as a commercial investment rather than an aid programme, and each began from demand conditions that Bangladesh's survey data now matches or exceeds.

The unit economics support the same conclusion domestically. Everyday retrofits such as LED lighting, water-saving fixtures, and efficient fans recover their cost within roughly two years; larger investments in solar, insulation, and efficient cooling reduce lifetime energy or water use by 20 to 60 percent. This is the return profile of a self-sustaining blended product, not a permanently subsidized one.

For banks and development finance institutions. The first-mover product is a green construction loan bundled with a certified-contractor network and verified materials, priced below conventional mortgages and led by the two features with the clearest payback: solar and insulation. Credit assessment will need to be adapted before this scales; traders and small business owners constitute over half the target market, and their cash flows do not fit salaried-borrower scoring models. Two execution risks deserve explicit management: stated demand will soften at the point of sale, which argues for demonstration homes and community-level pilots that exploit the finding that nearly 60 percent of households would adopt after seeing a neighbour do so; and certification must be third-party and credible from the outset, since the price premium households expect depends entirely on trust in the label.

For developers, contractors, and manufacturers. The mason is the gatekeeper of this market. Training and certification programmes for contractors are a precondition for lending at scale, and firms that build certified delivery capacity early will capture the bundled-finance channel. Import dependence in green materials creates a parallel manufacturing opportunity; local production of blocks, fixtures, and components would shorten paybacks and reduce loan sizes across the market.

For donors and policymakers. The data indicate that concessional capital is best deployed to de-risk the delivery system rather than to subsidize demand: blended first-loss structures for early green loan portfolios, support for contractor certification, and backing for community-scale infrastructure, which 90.8 percent of households support in forms such as shared solar rooftops and communal rainwater systems. Regional tailoring matters: solar and storage where the grid is weak, water systems where salinity is advancing, and insulation and reflective roofing where urban heat is most severe.

The evidence base for green affordable housing in Bangladesh has reached the point where the constraint is no longer analytical. Households have stated their preference at rates that exceed the benchmarks from markets where this model has already scaled commercially. The next move belongs to capital.

The Affordable Green Housing Market Assessment was conducted by Innovision Consulting Private Limited for IFC. For inquiries: info@innovision-bd.com

Author: Md. Golam Rabbi Anik, Project Coordinator, Innovision Consulting

.png)