A farmer prepares his pond for the season. He buys feed, stocks fingerlings, and hires labor. He invests nearly everything into the next six months. Then a heatwave hits. Water temperature rises, oxygen levels drop, and fish begin to die. Within days, months of work can be lost.

This is not an isolated story. It reflects the growing reality of climate risk in Bangladesh.

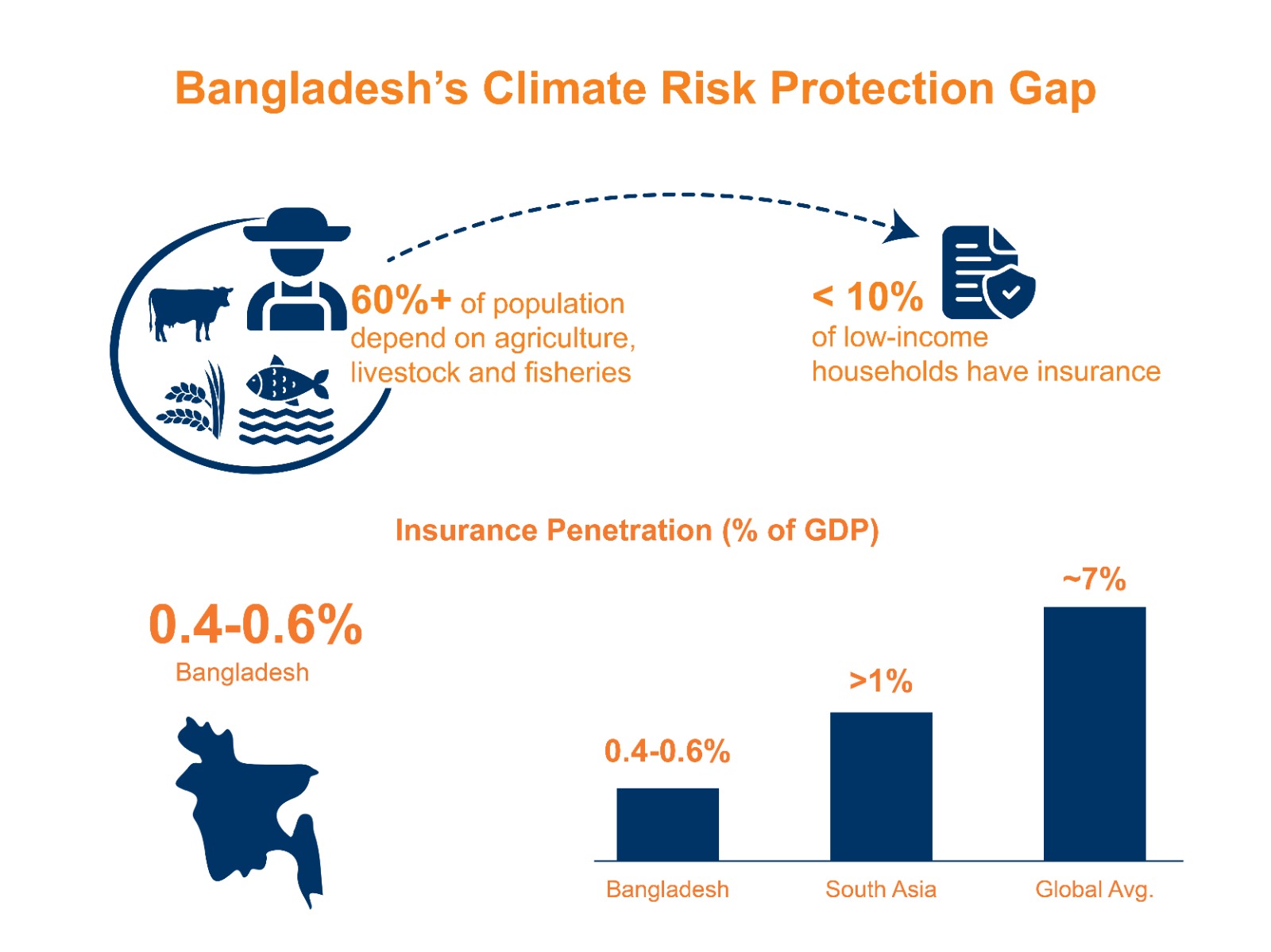

More than 60 percent of the population depends on climate-sensitive livelihoods such as agriculture, livestock, and fisheries. Yet insurance penetration in Bangladesh remains very low, around 0.4 to 0.6 percent of GDP. The global average is about 7 percent, and even South Asia exceeds 1 percent. At the household level, less than 10 percent of low-income families have access to formal insurance.

The gap between risk and protection is clear. The question is not whether agricultural insurance is needed, but which model can work at scale.

Microinsurance was designed to protect low-income households through small, affordable coverage. In agriculture, it covers crops against floods and droughts, livestock against mortality and disease, and aquaculture against heat, rainfall, and cold stress.

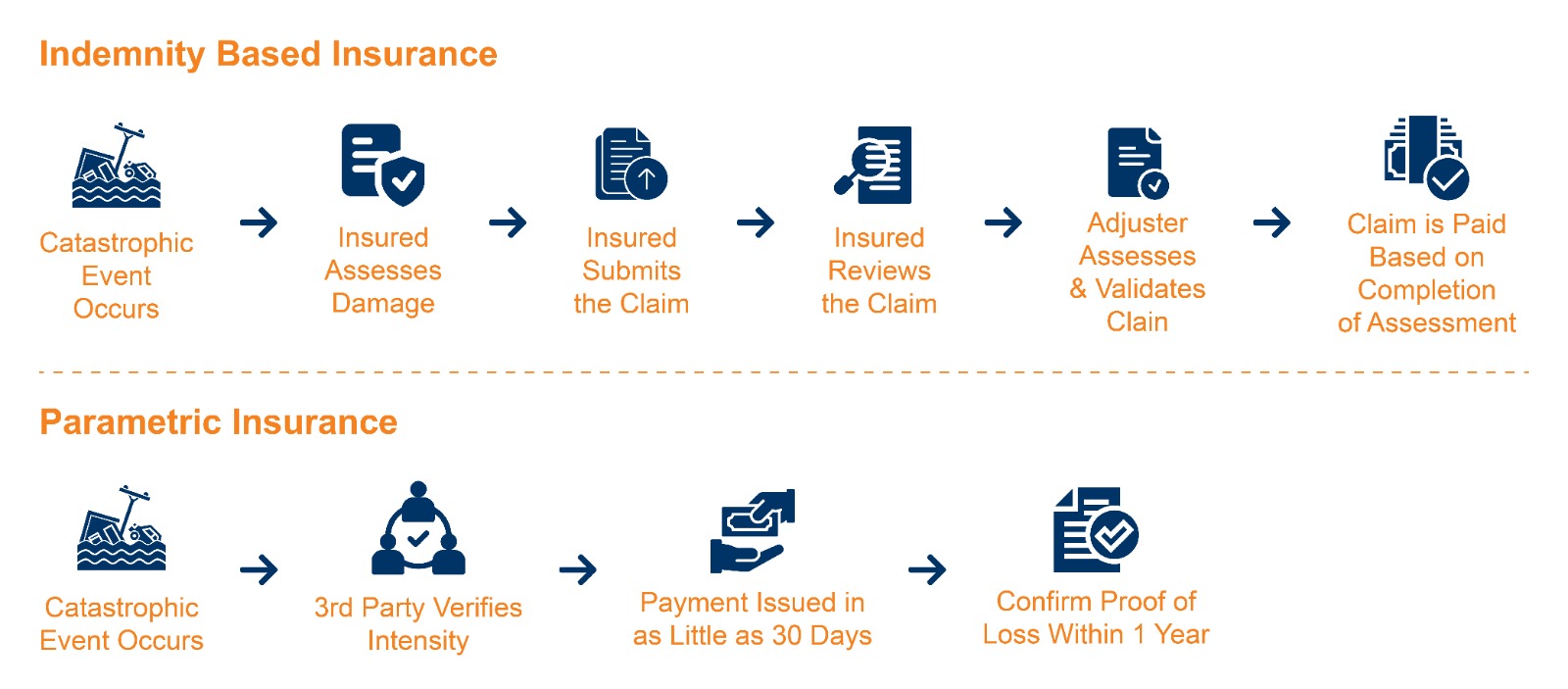

Most agricultural insurance in Bangladesh follows an indemnity-based model. Farmers report losses, surveyors inspect damage, and compensation is calculated based on measured loss. While this appears fair, it creates structural challenges in smallholder contexts.

Expense ratios in traditional agriculture microinsurance often exceed 40–50 percent. Agent commissions typically range from 10–15 percent. Manual enrollment, field inspections, and administrative overhead drive up costs. In some cases, inspection expenses exceed the value of the claim itself.

Payouts are also slow. Verification can take weeks or months, limiting the usefulness of insurance during emergencies. Because this system depends heavily on field manpower, scaling becomes expensive and difficult. Many programs remain small pilots and donor-supported rather than commercially sustainable.

The constraint is not farmer demand. It is the structure of the model.

Parametric (index-based) microinsurance changes the logic of insurance. Instead of insuring the loss itself, it insures the event that causes the loss.

Compensation is triggered automatically when a predefined environmental parameter, such as rainfall or temperature, crosses a specific threshold. These thresholds are designed using historical climate data to ensure a strong correlation with production loss.

The operational flow is straightforward. Farmers enroll digitally or through aggregator agents, with geolocation linking their farms to specific weather grids. Insurers monitor satellite data or weather station feeds in real time. If a trigger, such as temperature exceeding a defined level during a critical growth stage, is breached, payouts are automatically transferred to the farmer’s mobile wallet, such as bKash or Nagad. No individual loss assessment is required.

By removing field inspections after product design, parametric models lower administrative costs, improve transparency, and significantly accelerate payouts.

Aquaculture has long been considered difficult to insure because underwater stock losses are hard to verify. Yet it represents substantial working capital exposure for farmers.

Under the Bangladesh Microinsurance Market Development Programme (BMMDP), implemented by Swisscontact and funded by the Swiss Agency for Development and Cooperation (SDC), Innovision partnered with Green Delta Insurance PLC to develop Bangladesh’s first parametric microinsurance product for fisheries and aquaculture.

The product covers excessive heat, excessive rainfall, and low temperature. Triggers were calibrated using 30 years of sub-district-level data from the Bangladesh Meteorological Department to ensure actuarial robustness. For example, if temperature exceeds 35°C for a defined number of consecutive days during a sensitive growth period, payouts are activated automatically.

More than 1,000 farmers in Mymensingh and Khulna were engaged through over 50 courtyard sessions. The product helped protect average working capital investments of approximately USD 2,000 per production cycle per farmer. Distribution, premium collection, and claims disbursement are now operated by Green Delta, demonstrating operational viability beyond pilot testing.

Parametric models reduce administrative cost, accelerate payouts, limit disputes, and enable digital scale. However, they introduce basis risk, the possibility that a farmer experiences loss but the index does not trigger, or vice versa. Reducing basis risk requires dense weather station networks, strong historical data, and localized calibration.

Bangladesh already has important building blocks: decades of weather data, expanding digital payment systems, early pilot experience, and increasing regulatory awareness. Strengthening automated weather stations, improving data integration, and clarifying index-based regulatory frameworks will be essential for further scale.

Microinsurance alone cannot absorb catastrophic nationwide shocks. Complementary sovereign disaster risk financing mechanisms, such as sovereign parametric coverage or catastrophe bonds, may be needed to manage systemic risk. Between 2025 and 2030, coordinated action across data systems, insurers, regulators, and public institutions will determine whether agricultural insurance remains fragmented or becomes a scalable resilience instrument.

The transition from indemnity-based models to parametric microinsurance is not a technical preference. It is a structural necessity.

Traditional models are expensive, slow, and difficult to scale. Parametric models offer speed, transparency, and cost efficiency. When supported by strong data systems, regulatory clarity, and aligned institutions, they can move beyond pilots and become part of a national climate risk financing architecture.

Bangladesh’s agricultural future will depend not only on productivity, but on how effectively climate risk is managed. Parametric microinsurance offers a practical pathway toward faster recovery, stronger working capital protection, and a more resilient rural economy.

Author: Tahmeed Rifa, a Senior Associate in the Inclusive Financia Solutions (IFS) Portfolio at Innovision Consulting.

.png)